[ad_1]

[gpt3] a new article in English that is SEO-optimized and incorporates as many relevant keywords as possible. The article should be based on the information provided in the existing post content. Additionally, please include a dedicated FAQ section and a conclusion section to enhance the reader’s experience

In the latest episode of his Blockchain Gaming World podcast, editor-in-chief Jon Jordan talks to George Isichos, head of research at Game7 DAO, which has released its State of Web3 Gaming report.

Check out the report here.

This interview has been edited for length and clarity.

Can you give us a bit of background about yourself?

George Isichos: My blockchain gaming story starts in 2018. I joined a team of people trying to build a very rough version of Oblivion onchain. Blockchain gaming is close to six years old right now. For me, that’s amazing.

I have been with Game7 for a bit less than two years. I have been involved in a number of things, including research-related, grants-related, and helping this initiative grow. Prior to that I had some experience with working in the consulting sector with banks and energy companies, but at some point I saw the light and yeah, I’m an excited participant of the blockchain gaming market.

So we’re going to go through some of the graphs in the report but to begin with can you explain why you didn’t use any onchain data?

Yes. That’s a very valid question. It’s a number of reasons, actually. Number one, there have been some great reports and great research initiatives and databases to try to better understand onchain activity. We tried as a matter of diversity and just contributing to the public sphere to just do something different. If we try to dive into the composition of onchain data right now, we will see that onchain can mean something totally different for different games.

A game might say you can fund your account using Bitcoin, which on paper is using a blockchain. A game might say, all my in-game assets are NFTs. A game might say the outcome of your fight with your opponent now is logged on a specific blockchain. And a game might say, every movement you’re making on a game, it can be verified on a chain. So these are all blockchain games. But if you try to compare those games, you’re comparing apples and oranges.

The last point would be that I think we’re a bit early. Onchain data is a fantastic opportunity for us in the future to learn more about the gamers behavior and hopefully optimize for the experience of gamers. But it might be too early. So we’re saying to people, there is no right or wrong. Just look at this data as you’re also observing onchain information. I think we need both sides of the story to get a more holistic understanding of the space.

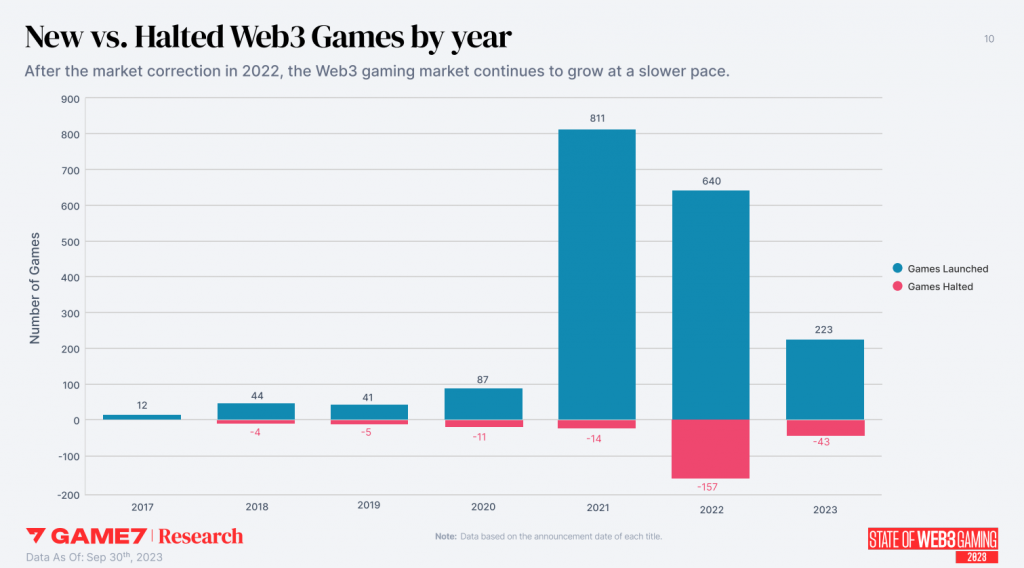

So the first graph is the number of new games announced since 2017.

The reason why first of all we started at this point is because I want to stress that blockchain gaming is not new. We have new assumptions, new ideas, new business models, new things to be excited about, but this has been an ongoing effort.

It’s also good to see that blockchain gaming is growing, if at a slower pace. It will be interesting to see how the recent market activity might impact this chart moving to the first quarter of 2024.

Looking at the geographical breakdown of teams, what can you say about this?

In this chart we’re tracking the number of game development teams. Also this chart refers to the new games per year. It gives a snapshot of the yearly activity. So for 2023, we had one third from the US, close to one third from South Korea, which is a big change. And Japan is also having a big jump. Asia is not a surprise in the gaming world – Asia is a big player, of course. I would say it’s not normal to not have Asian countries being a key driver for growth.

Also, you can argue that the lack of friendliness from the US currently might be a key driver for teams outside of the US to say, “OK, here’s an opportunity for us”. Because we see on a high level that APAC has more blockchain game development teams than the US right now, which to me, it’s very interesting.

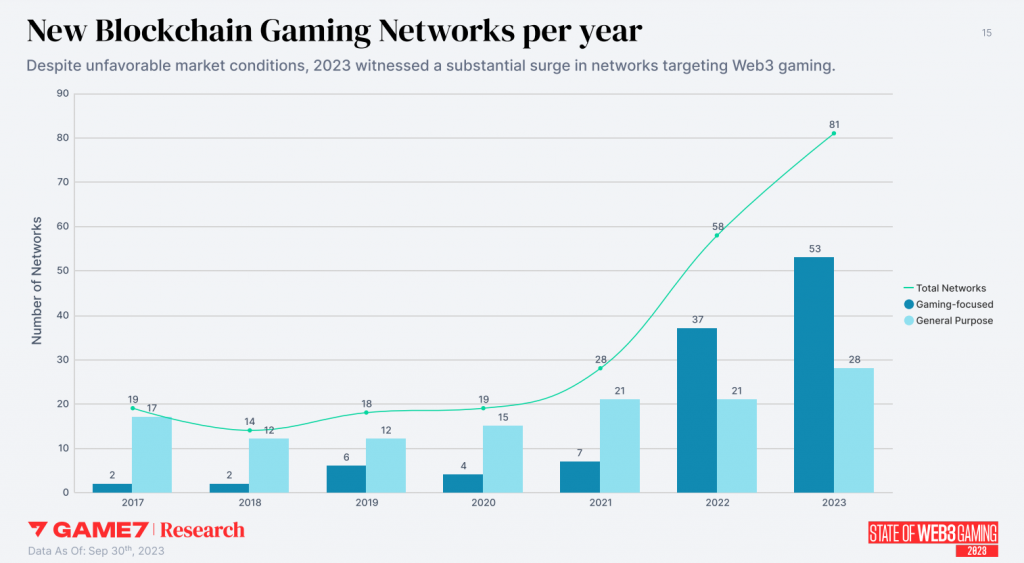

In this chart we’re looking at newly announced blockchains, which are growing quickly.

Yes, the number is huge. We can try to explain it in a couple of ways. I think number one, the previous funding definitely fuelled some of this development activity from previous years and these teams, they had to continue building, they had funding, they had a plan. Despite of course the unfavorable market conditions, they continued to build and at some point they launched a network or they announced a network.

I think also a key driver would be the maturity of blockchain frameworks, so frameworks to allow any game dev to deploy their own chain. We have Avalanche subnets, Polygon supernets, we have the Cosmos SDK, you have Arbitrum Nitro. There are many options for game developers to just take a popular and well-established protocol and fork it to their own needs, either as layer 2 or layer 3, or even layer 1.

Launching a chain that has specific characteristics is still a big challenge and creating an ecosystem is a huge challenge, but technically speaking, having your own chain to the needs of your own environment in game is not that hard anymore than there are many, many solutions.

Looking at the platform breakdown of games, it’s interesting that browser is high in 2023.

There are many ways to explain the outcomes. Some takeaways would be that mobile continues to be a great choice for wealthy game developers. I think the concept of micro transactions in hypercasual games, you play on the subway, I think this narrative works. And game developers, they do definitely believe in it. That’s why we see mobile being the most popular platform for the past two years.

When it comes to browsers, I think browsers are popular in the web3 space because it’s easier to build a browser game than a PC or a mobile one. So as an early experimentation, I think it makes sense for many people to start by browser. There’s also another interesting trend that is the space of fully onchain games, which again is a very specific subset of web3 games.

Also, a lot of big tech doesn’t like blockchain. If tomorrow morning, Apple and Google and Epic and Steam say, “okay, I’m fine with web3”, things would be different. Currently this graph highlights an interesting mix of pressure from both the development pains and also the distribution challenge.

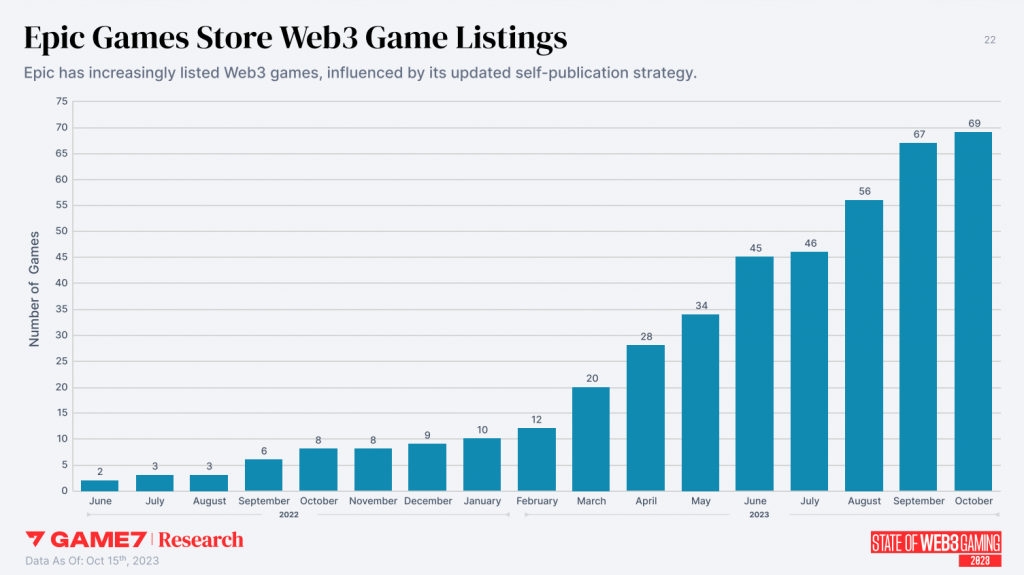

Of course, Epic is the place for blockchain PC games to find distribution.

When it comes to Epic, I think the picture is definitely positive but I’m not sure that there are no restrictions for blockchain games on Epic so PC developers maybe have to release a web2 version on Steam, and web3-lite version on Epic and the full game via their launcher.

For me, that’s not super sustainable. You can’t really scale an ecosystem if every game development team has to maintain two or three versions. And that’s why the whole web3 distribution part and the native distribution of tools remains a critical challenge for the space. Solving the distribution challenge is still a big challenge.

Why are fully onchain games important?

For me, activity on fully onchain games is not so much about gaming, but it’s more about the whole ownerless or fully autonomous social system. It doesn’t have to be, for example, a game, just a system with rules and with evolution that is not defined by a single guy pressing the button. That’s why we at Game7 have supported with grants many teams building with all the existing tools in the fully onchain space, because it’s a fantastic way to innovate and stress test the blockchain stack.

It doesn’t matter if it will lead to the next free-to-play idea that will create billions for the gaming industry. I don’t think that’s the point. There’s a good chance though that something from this process will end up being a great use case that also has commercial potential.

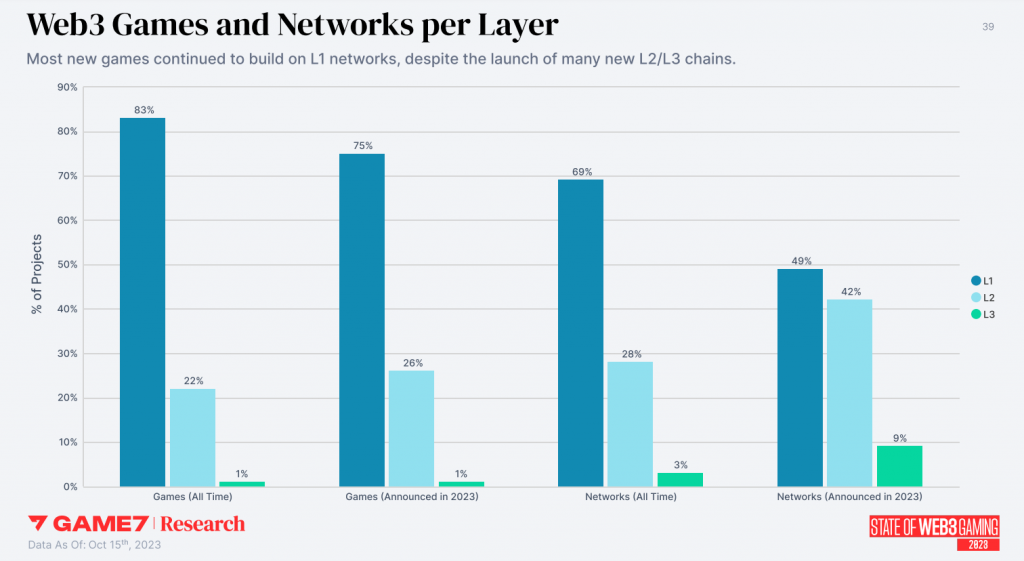

So this graph is complex. Can you explain what is going on?

Yes. So on the left side, we’re seeing the layer that each blockchain game has picked today. That’s an all-time snapshot. So 83% of games are using layer one networks. The reason why this sums more than 100 is because specific games might use more than one chain, and these changes might be of a different kind.

The key way to read this is that the vast majority of blockchain game developers right now don’t really care about the layer. They might find great potential in the promise of using a layer 2 versus a layer 1, but relying on existing ecosystems like the Ethereum ecosystem instead of spinning up their own ecosystem.

Game developers are focused on selecting the game that makes sense for their game stack and their business plans. They say “I need the best chain for my game”.

On the network’s front, we’re seeing strong interest on layer 2 and layer 3 networks. So, engineering teams are launching more layer 2s and layer 3s, but so far game developers, they are interested in the layer 2 space but they currently heavily rely on layer 1 networks

How did you come up with the data for this migration graph?

Let’s say you’re building on Polygon and you say, I want to also integrate Avalanche and BNB, while also keeping Polygon, we will count this as an expansion on our database, not as a migration. Because in some cases, moving between EVM chains might be like five lines of code, so I don’t think it makes sense. But when you’re saying, scrap the existing work, I’m going to launch on a new ecosystem. I think this is an important decision for game developers. But many migrations are not public, so I think the actual number is bigger than this

Trying to read behind the numbers, if you asked me one or two years ago, I would say “whoever is paying more gets the game”; the key reason was the financial support developers received from the ecosystem.

Now, however, the key decision criteria is the readiness of the chain to function. So if a game dev has the content ready in the next six months and they need a performing environment so they can launch their own token, launch their NFTs and have an economy to eventually make money and grow the ecosystem. They need something where it works or has the promise to work at a specific level of scale.

Check out the full 61 page report here.

[/]

[ad_2]

Source link